Property Purchase Taxes in Spain: Complete Official Breakdown 2026 | Mario Premium Property Services

ARTICLE 2 — COSTA BLANCA SUR · MARCH 2026

Buying a €350,000 property in Spain: budget €400,000 — here is the official breakdown

Why this article is essential

One of the most common mistakes — particularly among international buyers — is negotiating the purchase price while completely overlooking associated taxes and costs. In the Valencian Community (Costa Blanca), additional costs range between 11% and 14% of the purchase price. Underestimating them can derail a deal that is already agreed.

This breakdown is based on official legislation current as of March 2026, specifically for the Valencian Community (Comunitat Valenciana).

BLOCK 1 · Resale Property — €350,000

Applicable tax: ITP (Transfer Tax — Impuesto sobre Transmisiones Patrimoniales)

Legal basis: Law 13/1997, 23 December, Generalitat Valenciana. Current general rate 2026: 10%.

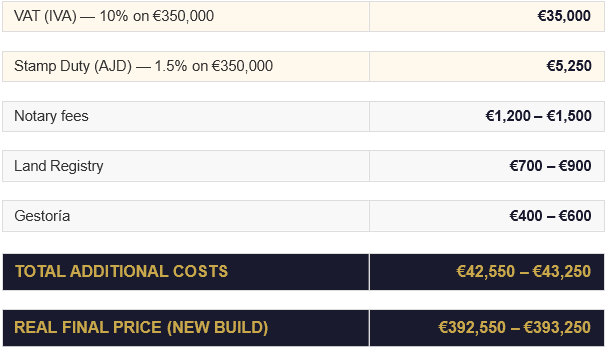

BLOCK 2 · New Build — €350,000

Applicable taxes: VAT (IVA) + Stamp Duty (AJD — Actos Jurídicos Documentados)

VAT legal basis: Article 91.One.7, Law 37/1992. Reduced rate of 10% for residential property.

Stamp Duty legal basis: Law 13/1997, Generalitat Valenciana. General rate 1.5%. (Reduced 0.1% rate applies only to primary residence with specific income requirements.)

BLOCK 3 · Key Points Every Buyer Must Know

- ITP is a regional tax. Each autonomous community sets its own rate. Valencia: 10%. Madrid: 6%. Always verify the region.

- Notary and Land Registry fees are national fixed scales (RD 1427/1989) — non-negotiable.

- Stamp Duty (AJD) only applies to new build (first sale). Resale properties do NOT pay AJD.

- Gestoría fees are negotiable. Always get at least 2–3 quotes.

- If financing with a mortgage: since November 2018 (RDL 17/2018), the bank — not the buyer — pays the AJD on the mortgage deed.

- Non-resident investors: the purchase tax process is identical. The difference arises in subsequent rental income taxation (IRNR, Form 210).

📚OFFICIAL VERIFIED SOURCES

- Spanish Tax Agency — Reduced VAT on housing: www.agenciatributaria.es | Law 37/1992, Art. 91

- Generalitat Valenciana — ITP and Stamp Duty: www.gva.es | Law 13/1997, 23 December

- Ministry of Finance — Royal Legislative Decree 1/1993 (Consolidated ITP and AJD)

- Notary and Registry Scales — Royal Decree 1427/1989

- Bank of Spain — RDL 17/2018, Mortgage Stamp Duty: www.bde.es

- Registradores de España — Quarterly statistics: www.registradores.org

Document prepared with official data verified as of March 2026. This article is for informational purposes only. For individualised tax advice, consult a qualified tax advisor.

📧 Email: servicios@mariopremium.es

📱 Phone: +34 613 53 51 25

📍 Office: C/ Comunidad Castellano-Manchega, 23 – 03190 Pilar de la Horadada, Alicante

Languages: English, Spanish, Dutch, Polish

PUBLISHED: 20 March 2026 | UPDATED: 20 March 2026

AUTHOR: Mario Premium Legal Team

CATEGORY: Informative

SHARE THIS ARTICLE:

Facebook | WhatsApp | Email